Handling Missing Response¶

Because of the generative nature of the exponential smoothing models, they can naturally deal with missing response during the training process. It simply replaces observations by prediction during the 1-step ahead generating process. Below users can find the simple examples of how those exponential smoothing models handle missing responses.

[1]:

import pandas as pd

import numpy as np

import orbit

import matplotlib.pyplot as plt

from orbit.utils.dataset import load_iclaims

from orbit.diagnostics.plot import plot_predicted_data, plot_predicted_components

from orbit.utils.plot import get_orbit_style

from orbit.models import ETS, LGT, DLT

from orbit.diagnostics.metrics import smape

plt.style.use(get_orbit_style())

%load_ext autoreload

%autoreload 2

%matplotlib inline

[2]:

orbit.__version__

[2]:

'1.1.4.6'

Data¶

[3]:

# can also consider transform=False

raw_df = load_iclaims(transform=True)

raw_df.dtypes

df = raw_df.copy()

df.head()

[3]:

| week | claims | trend.unemploy | trend.filling | trend.job | sp500 | vix | |

|---|---|---|---|---|---|---|---|

| 0 | 2010-01-03 | 13.386595 | 0.219882 | -0.318452 | 0.117500 | -0.417633 | 0.122654 |

| 1 | 2010-01-10 | 13.624218 | 0.219882 | -0.194838 | 0.168794 | -0.425480 | 0.110445 |

| 2 | 2010-01-17 | 13.398741 | 0.236143 | -0.292477 | 0.117500 | -0.465229 | 0.532339 |

| 3 | 2010-01-24 | 13.137549 | 0.203353 | -0.194838 | 0.106918 | -0.481751 | 0.428645 |

| 4 | 2010-01-31 | 13.196760 | 0.134360 | -0.242466 | 0.074483 | -0.488929 | 0.487404 |

[4]:

test_size=52

train_df=df[:-test_size]

test_df=df[-test_size:]

Define Missing Data¶

Now, we manually created a dataset with a few missing values in the response variable.

[5]:

na_idx = np.arange(53, 100, 1)

na_idx

[5]:

array([53, 54, 55, 56, 57, 58, 59, 60, 61, 62, 63, 64, 65, 66, 67, 68, 69,

70, 71, 72, 73, 74, 75, 76, 77, 78, 79, 80, 81, 82, 83, 84, 85, 86,

87, 88, 89, 90, 91, 92, 93, 94, 95, 96, 97, 98, 99])

[6]:

train_df_na = train_df.copy()

train_df_na.iloc[na_idx, 1] = np.nan

Exponential Smoothing Examples¶

ETS¶

[7]:

ets = ETS(

response_col='claims',

date_col='week',

seasonality=52,

seed=2022,

estimator='stan-mcmc'

)

ets.fit(train_df_na)

ets_predicted = ets.predict(df=train_df_na)

2024-03-19 23:38:16 - orbit - INFO - Sampling (CmdStanPy) with chains: 4, cores: 8, temperature: 1.000, warmups (per chain): 225 and samples(per chain): 25.

LGT¶

[8]:

lgt = LGT(

response_col='claims',

date_col='week',

estimator='stan-mcmc',

seasonality=52,

seed=2022

)

lgt.fit(df=train_df_na)

lgt_predicted = lgt.predict(df=train_df_na)

2024-03-19 23:38:17 - orbit - INFO - Sampling (CmdStanPy) with chains: 4, cores: 8, temperature: 1.000, warmups (per chain): 225 and samples(per chain): 25.

DLT¶

[9]:

dlt = DLT(

response_col='claims',

date_col='week',

estimator='stan-mcmc',

seasonality=52,

seed=2022

)

dlt.fit(df=train_df_na)

dlt_predicted = dlt.predict(df=train_df_na)

2024-03-19 23:38:21 - orbit - INFO - Sampling (CmdStanPy) with chains: 4, cores: 8, temperature: 1.000, warmups (per chain): 225 and samples(per chain): 25.

Summary¶

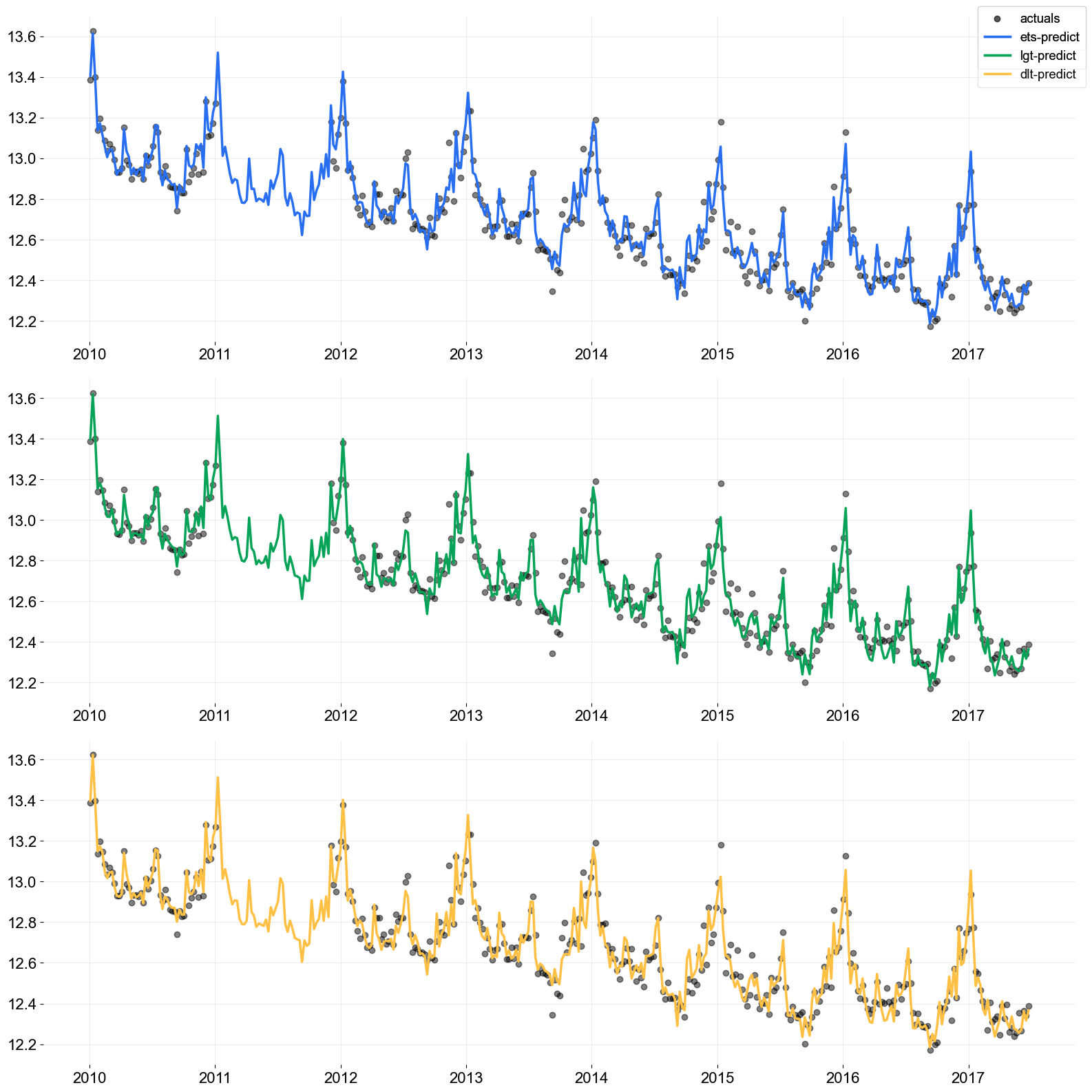

Users can verify this behavior with a table and visualization of the actuals and predicted.

[10]:

train_df_na['ets-predict'] = ets_predicted['prediction']

train_df_na['lgt-predict'] = lgt_predicted['prediction']

train_df_na['dlt-predict'] = dlt_predicted['prediction']

[11]:

# table summary of prediction during absence of observations

train_df_na.iloc[na_idx, :].head(5)

[11]:

| week | claims | trend.unemploy | trend.filling | trend.job | sp500 | vix | ets-predict | lgt-predict | dlt-predict | |

|---|---|---|---|---|---|---|---|---|---|---|

| 53 | 2011-01-09 | NaN | 0.152060 | -0.127397 | 0.085412 | -0.295869 | -0.036658 | 13.519096 | 13.512083 | 13.512583 |

| 54 | 2011-01-16 | NaN | 0.186546 | -0.044015 | 0.074483 | -0.303546 | 0.141233 | 13.281033 | 13.279732 | 13.278579 |

| 55 | 2011-01-23 | NaN | 0.169451 | -0.004795 | 0.074483 | -0.309024 | 0.222816 | 13.011531 | 13.010502 | 13.013743 |

| 56 | 2011-01-30 | NaN | 0.079300 | 0.032946 | -0.005560 | -0.282329 | -0.006710 | 13.056016 | 13.068143 | 13.061067 |

| 57 | 2011-02-06 | NaN | 0.060252 | -0.024213 | 0.006275 | -0.268480 | -0.021891 | 12.992839 | 13.015295 | 13.007281 |

[12]:

from orbit.constants.palette import OrbitPalette

# just to get some color from orbit palette

orbit_palette = [

OrbitPalette.BLACK.value,

OrbitPalette.BLUE.value,

OrbitPalette.GREEN.value,

OrbitPalette.YELLOW.value,

]

[13]:

pred_list = ['ets-predict', 'lgt-predict', 'dlt-predict']

fig, axes = plt.subplots(len(pred_list), 1, figsize=(16, 16))

for idx, p in enumerate(pred_list):

axes[idx].scatter(train_df_na['week'], train_df_na['claims'].values,

label='actuals' if idx == 0 else '', color=orbit_palette[0], alpha=0.5)

axes[idx].plot(train_df_na['week'], train_df_na[p].values,

label=p, color=orbit_palette[idx + 1], lw=2.5)

fig.legend()

fig.tight_layout()

First Observation Exception¶

It is worth pointing out that the very first value of the response variable cannot be missing since this is the starting point of the time series fitting. An error message will be raised when the first observation in response is missing.

[14]:

# DO NOT RUN

# na_idx2 = list(na_idx) + [0]

# train_df_na2 = train_df.copy()

# train_df_na2.iloc[na_idx2, 1] = np.nan

# ets.fit(train_df_na2)