Quick Start¶

This session covers topics:

a forecast task on iclaims dataset

a simple Bayesian ETS Model using

CmdStanPyposterior distribution extraction

tools to visualize the forecast

Load Library¶

[1]:

%matplotlib inline

import matplotlib.pyplot as plt

import orbit

from orbit.utils.dataset import load_iclaims

from orbit.models import ETS

from orbit.diagnostics.plot import plot_predicted_data

[2]:

print(orbit.__version__)

1.1.4.6

Data¶

The iclaims data contains the weekly initial claims for US unemployment (obtained from Federal Reserve Bank of St. Louis) benefits against a few related Google trend queries (unemploy, filling and job) from Jan 2010 - June 2018. This aims to demo a similar dataset from the Bayesian Structural Time Series (BSTS) model (Scott and Varian 2014).

Note that the numbers are log-log transformed for fitting purpose and the discussion of using the regressors can be found in later chapters with the Damped Local Trend (DLT) model.

[3]:

# load data

df = load_iclaims()

date_col = 'week'

response_col = 'claims'

df.dtypes

[3]:

week datetime64[ns]

claims float64

trend.unemploy float64

trend.filling float64

trend.job float64

sp500 float64

vix float64

dtype: object

[4]:

df.head(5)

[4]:

| week | claims | trend.unemploy | trend.filling | trend.job | sp500 | vix | |

|---|---|---|---|---|---|---|---|

| 0 | 2010-01-03 | 13.386595 | 0.219882 | -0.318452 | 0.117500 | -0.417633 | 0.122654 |

| 1 | 2010-01-10 | 13.624218 | 0.219882 | -0.194838 | 0.168794 | -0.425480 | 0.110445 |

| 2 | 2010-01-17 | 13.398741 | 0.236143 | -0.292477 | 0.117500 | -0.465229 | 0.532339 |

| 3 | 2010-01-24 | 13.137549 | 0.203353 | -0.194838 | 0.106918 | -0.481751 | 0.428645 |

| 4 | 2010-01-31 | 13.196760 | 0.134360 | -0.242466 | 0.074483 | -0.488929 | 0.487404 |

Train-test split.

[5]:

test_size = 52

train_df = df[:-test_size]

test_df = df[-test_size:]

Forecasting Using Orbit¶

Orbit aims to provide an intuitive initialize-fit-predict interface for working with forecasting tasks. Under the hood, it utilizes probabilistic modeling API such as CmdStanPy and Pyro. We first illustrate a Bayesian implementation of Rob Hyndman’s ETS (which stands for Error, Trend, and Seasonality) Model (Hyndman et. al, 2008) using CmdStanPy.

[6]:

ets = ETS(

response_col=response_col,

date_col=date_col,

seasonality=52,

seed=2024,

estimator="stan-mcmc",

stan_mcmc_args={'show_progress': False},

)

[7]:

%%time

ets.fit(df=train_df)

2024-03-19 23:42:10 - orbit - INFO - Sampling (CmdStanPy) with chains: 4, cores: 8, temperature: 1.000, warmups (per chain): 225 and samples(per chain): 25.

CPU times: user 42.9 ms, sys: 24.3 ms, total: 67.2 ms

Wall time: 613 ms

[7]:

<orbit.forecaster.full_bayes.FullBayesianForecaster at 0x2a5274b50>

[8]:

predicted_df = ets.predict(df=test_df)

[9]:

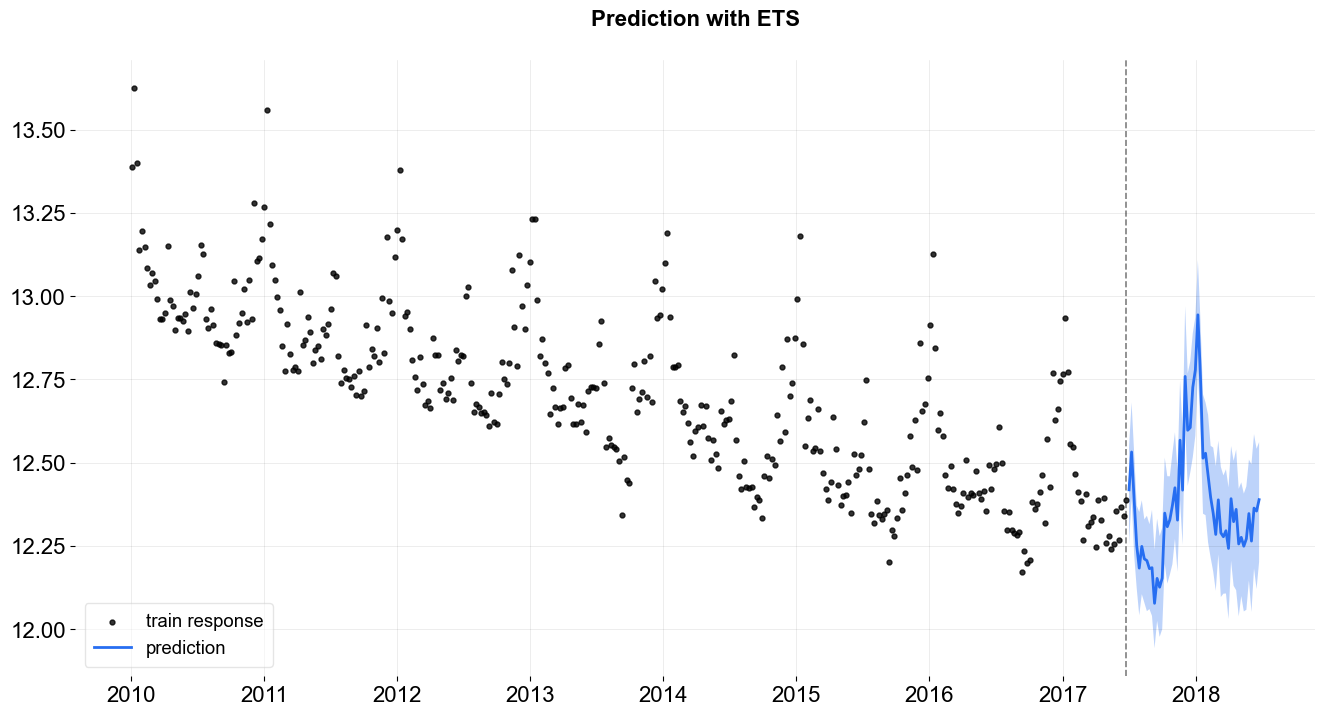

_ = plot_predicted_data(train_df, predicted_df, date_col, response_col, title='Prediction with ETS')

Extract and Analyze Posterior Samples¶

Users can use .get_posterior_samples() to extract posterior samples in an OrderedDict format.

[10]:

posterior_samples = ets.get_posterior_samples()

posterior_samples.keys()

[10]:

dict_keys(['l', 'lev_sm', 'obs_sigma', 's', 'sea_sm', 'loglk'])

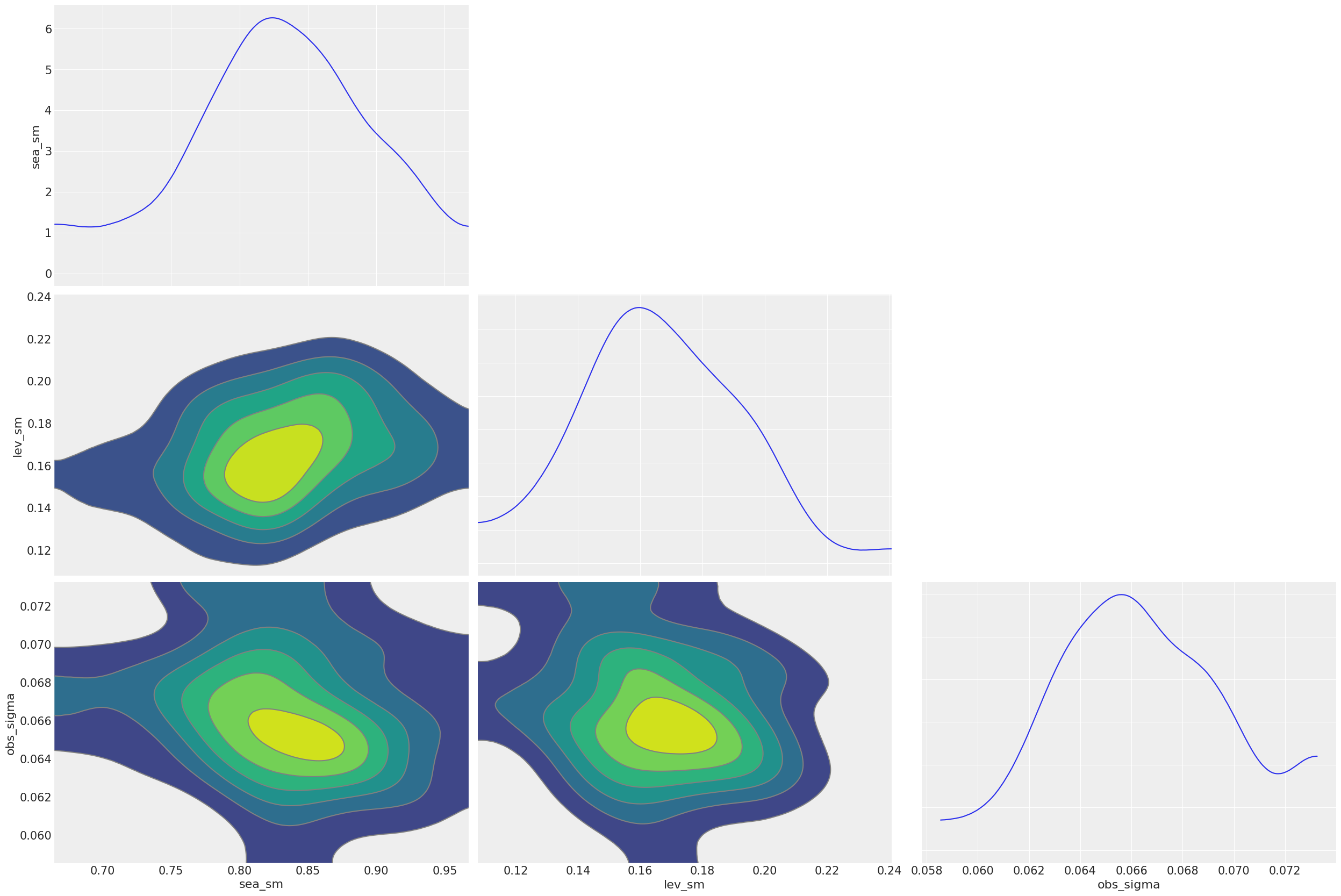

The extracted parameters posteriors are pretty much compatible diagnostic with arviz. To do that, users can set permute=False to preserve chain information.

[11]:

import arviz as az

posterior_samples = ets.get_posterior_samples(permute=False)

# example from https://arviz-devs.github.io/arviz/index.html

az.style.use("arviz-darkgrid")

az.plot_pair(

posterior_samples,

var_names=["sea_sm", "lev_sm", "obs_sigma"],

kind="kde",

marginals=True,

textsize=15,

)

plt.show()

For more details in model diagnostics visualization, there is a subsequent section dedicated to it.